Choosing between dollar-cost averaging (DCA) and lump sum investing (LSI) is similar to navigating a financial crossroads. Having experimented with both strategies, I’m eager to share my insights and experiences to help you make an informed decision.

Table of contents:

Dollar-Cost Averaging

Let’s start with the basics. Dollar-cost averaging (DCA) involves consistently investing a fixed amount of money at predetermined intervals, irrespective of market fluctuations.

The DCA Advantage

Dollar-cost averaging offers several key advantages:

- Mitigates market volatility: By spreading investments over time, DCA helps cushion the impact of market ups and downs.

- Discipline and consistency: It fosters the development of steady and consistent investment practices.

- Emotional resilience: The strategy eliminates the emotional fear associated with timing the market, as it focuses on the long-term average.

The DCA Myth

Although Dollar-Cost Averaging (DCA) has its benefits, it’s not a surefire strategy. Some people claim that DCA consistently beats investing a lump sum. However, it’s important to note that the belief in the market always bouncing back is not a certainty. If the market consistently rises, investing a lump sum might lead to better outcomes.

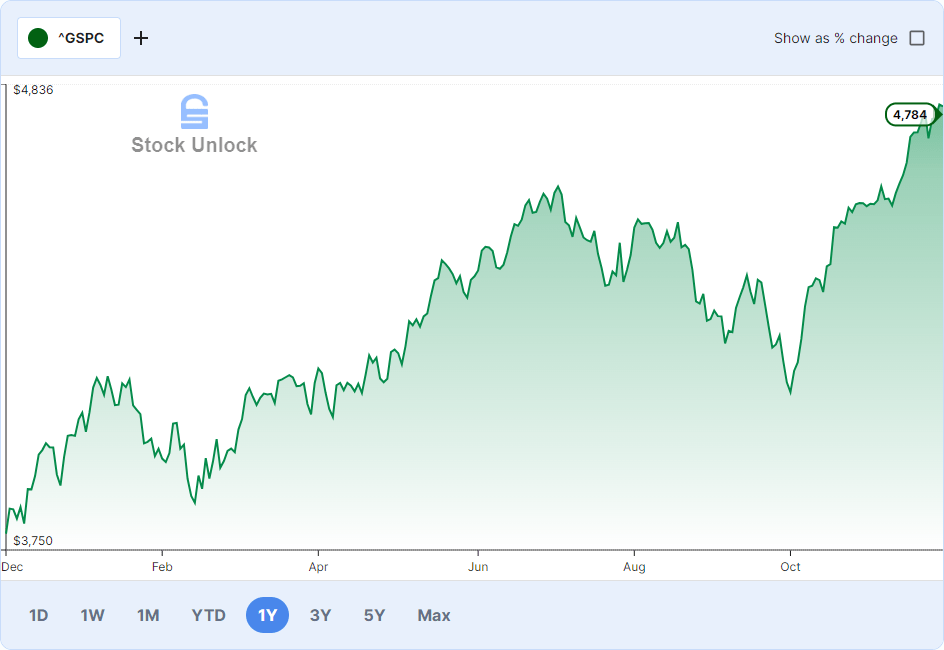

To demonstrate, let’s look at how DCA performs with an investment in the top 500 US companies represented by the S&P 500 over a year.

| Date | Value |

| Dec 01 2022 | $4087 |

| Jan 03 2023 | $3853 |

| Feb 01 2023 | $4070 |

| Mar 01 2023 | $3963 |

| Apr 03 2023 | $4102 |

| May 01 2023 | $4167 |

| Jun 01 2023 | $4183 |

| Jul 03 2023 | $4450 |

| Aug 01 2023 | $4579 |

| Sep 01 2023 | $4531 |

| Oct 02 2023 | $4285 |

| Nov 01 2023 | $4201 |

The average acquisition cost stands at $4125, yielding a 10.45% return relative to the current value of $4,556. Notably, a straightforward purchase of the S&P 500 index one year ago resulted in an 11.3% return. This comparison highlights that during a market recovery from a previous downturn, the use of dollar-cost averaging may cause you to miss out on the potentially more attractive momentum.

Lump Sum Investing

Now, let’s turn our attention to lump sum investing. Unlike DCA, where you invest fixed amounts at regular intervals, LSI involves deploying a significant sum of money in a single, one-time investment.

The LSI Advantage

Here is a list of the most important advantages of this approach.

- Provides immediate exposure to the market, and minimizes the risk of missing out on potential market gains.

- Enables you to enter the market at potentially lower prices.

- Simple and convenient, involving a one-time investment decision.

The LSI Dilemma

Although investing a lump sum offers the potential for greater returns, it also carries a considerable amount of risk. Opting for a lump sum strategy exposes you to market volatility without the benefit of incremental contributions over time. If the market takes a downturn shortly after you make your lump sum investment, it can have a substantial impact on your portfolio.

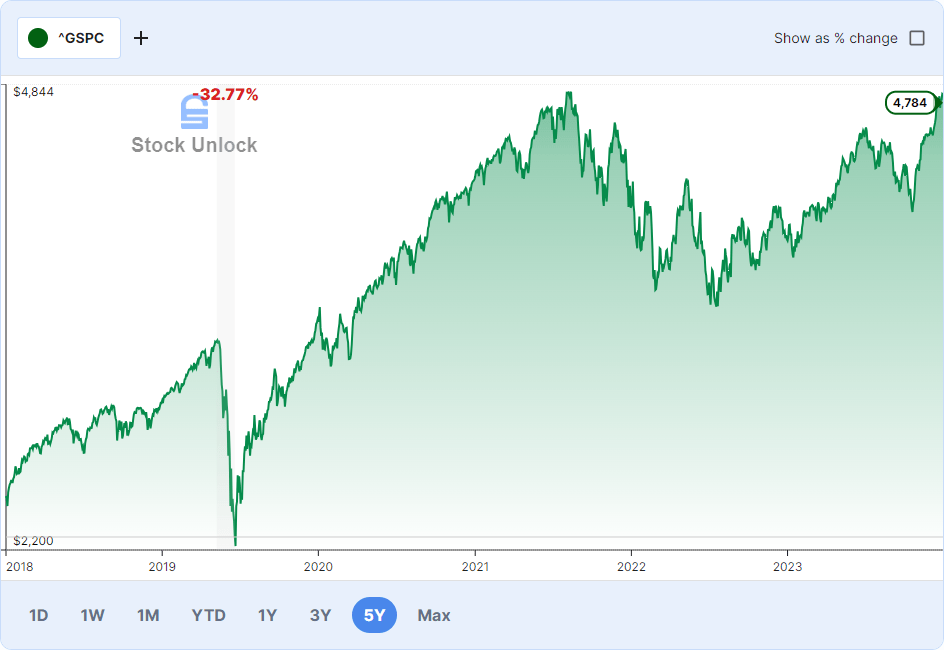

Consider the scenario of employing the Lump sum strategy at the beginning of 2020, just before the 30% drawdown triggered by the onset of the COVID-19 pandemic.

Although the market exhibited a relatively swift recovery, the fear of potential loss, especially if a significant portion of your net worth was invested, might force you to withdraw at an inopportune time, impacting your financial portfolio.

How to Find the Balance?

Choose by Goal

Deciding between dollar-cost averaging and lump-sum investing hinges on your financial goals, risk tolerance, and market outlook. Let’s dissect the decision-making process with a clear breakdown:

- Financial goals: If you have a long investment horizon and are aiming for steady wealth accumulation, DCA into an index might be your ally.

- Risk tolerance: If you can weather market storms without losing sleep, LSI could be your path to potential higher returns.

- Market outlook: A careful analysis of market trends and economic indicators can guide your decision. LSI might be more appealing in bullish markets.

The Right Choice for Individual Stocks

It’s essential to re-evaluate both approaches when dealing with individual stocks. Avoid dollar-cost averaging into a stock trading significantly above your assessed fair value. Instead, opt for a lump-sum approach when the stock aligns with your valuation.

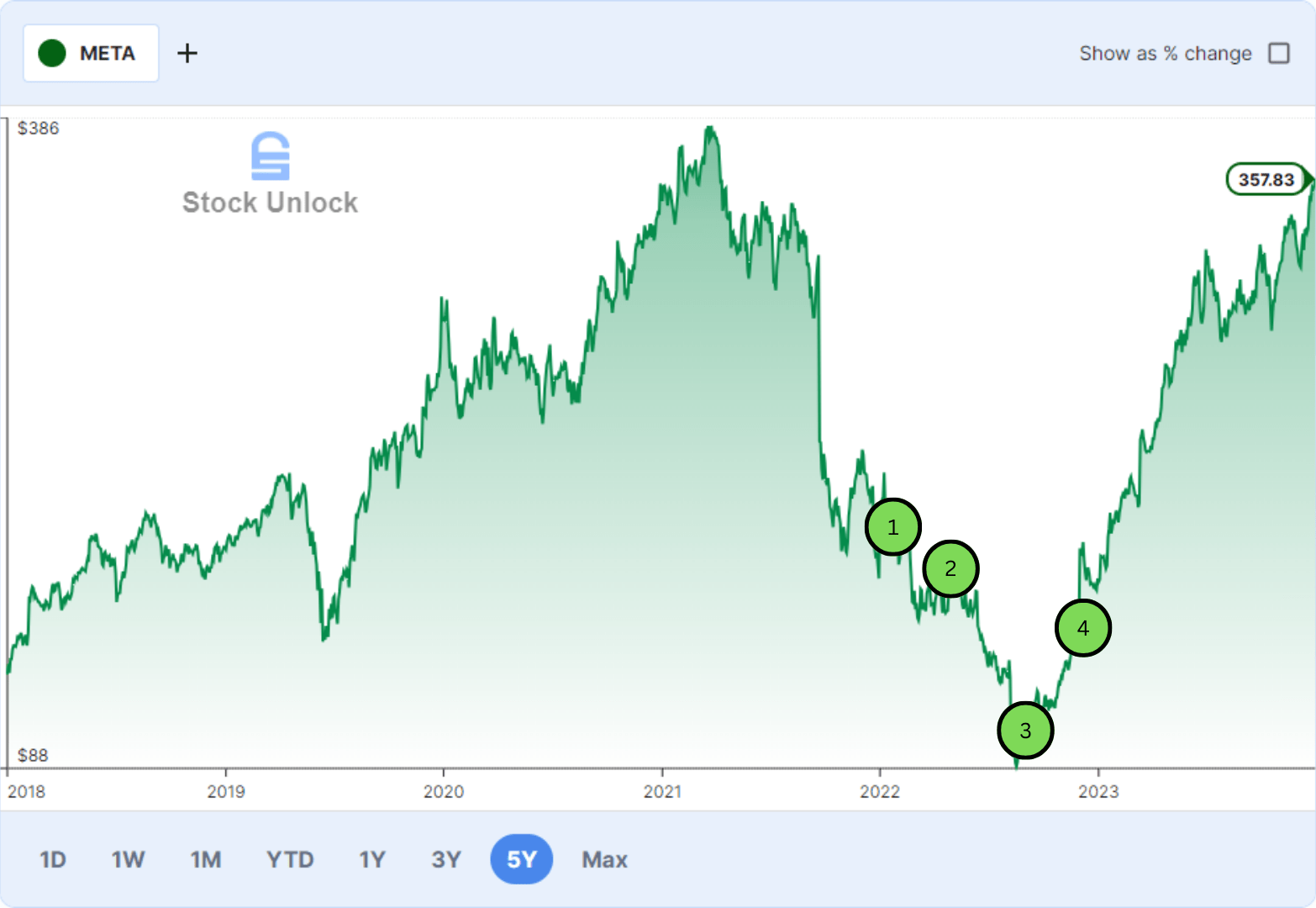

Simultaneously, consider a hybrid strategy combining lump-sum and DCA, we can take the META case as an example. If your fair value was $200, initiate a DCA at this price and subsequently employ a lump-sum approach at a lower price for potentially higher returns.

The Right Choice for ETFs

If you’re looking for an easy way to invest without diving deep into market research, here’s my personal suggestion: start by putting a lump sum into diversified indexes. Then, with each paycheck, consistently invest a set amount. This approach helps you enjoy the immediate gains of your investment while smoothing out the impact of market changes over time. It’s a strategy I’ve found to be balanced and effective.

Conclusion

In the dollar-cost averaging vs. lump sum investing debate, there’s no clear winner. Each strategy has its time and place. When applied wisely, each strategy can serve as a tool to build a position in the stock/ETF you want to own.

Leave a Reply